Now That You're Retired, Maximize Your Retirement Income

Those long-awaited Golden Years have arrived, and you're enjoying a well-deserved retirement. You've saved and invested wisely to provide a financial cushion, but making the most of your assets now -- maximizing your retirement income -- may require a brand new strategy. Where do you go from here?

Factor In the Variables

Investing during retirement can be uncharted terrain for many people. An appointment with your investment professional to reassess your portfolio can be crucial in helping you meet your changing needs. With uncertain variables such as longer life expectancies, the changing rate of inflation, and the possibility that you could outlive your retirement funds, you'll want to be sure your investments will keep up with you and outpace the cost of living.

Neglecting your investment strategy now could be costly. Inflation is one reason; even at a moderate 3% rate, inflation can substantially cut the purchasing power of your savings over 20 years. Another is that you may find your hard-earned cash dwindling too fast. A balanced portfolio of investments to maximize security while building needed profitability may be crucial to your financial security.

Keep Stocks Working for You

Many people believe that retirement means investing everything in low-return money market accounts1 or certificates of deposit (CDs). While these investments do offer little risk to principal, you should also consider the risks that (1) your assets will not keep pace with inflation and (2) you may outlive your assets. Although past performance is no guarantee of future results, stocks have historically outpaced inflation by the widest margin and have provided the strongest returns over the long term.2

A Focus on Yield

Along with some stock investments, a significant portion of your principal will likely be invested in fixed-income investments to provide a consistent stream of income. Depending on your needs, such investments may include high-quality corporate and government bonds, tax-exempt bonds, or high-yield "junk" bonds.3 How much risk (maturity and credit risk) you need to take with these investments depends in part on how much income you need. For example, if you can get by with a low annual return, you might be comfortable with high-quality, medium-term, fixed-income investments. But if you need to generate higher returns on your money, you'll need a longer-term strategy and will likely have to take on more risk.

You can buy individual government bonds of varying maturities and coupon rates to match your projected cash flow needs. In fact, this is how many insurance companies and banks manage cash flows to minimize interest rate risk. They first estimate a schedule of cash outflows and then buy securities "maturing" along the same schedule. You can use a similar strategy by buying bonds maturing (principal repaid) in one, two, and three years based on your expected cash needs in those years. You'll earn the stated rate of interest and likely have little risk of loss of principal, since you shouldn't need to sell the bonds before the scheduled due date. The rest of your bond portfolio may be invested in higher yielding, longer term investments.

| Now That You're Retired, Maximize Your Retirement Income | |||

| Security | Risk | Income | Growth Potential |

|---|---|---|---|

| 3-Month T-Bill | Low | Low | Lowest |

| Commercial Paper | Low | Low | Low |

| Dividend-Paying Stock | Medium | Low | Medium |

| Intermediate Bond | Medium | Medium | Low |

| Corporate Bond | Medium | Medium | Low |

| Convertible Stock | Medium | Medium | Low |

| High-Yield Bond | High | High | Medium |

| Growth Stock | High | Low | High |

| International Stock | High | Low | High |

Your Retirement Distribution

For many people, retirement is also a time to elect a distribution from their company pension and retirement savings plans. Many people may also begin taking distributions from an IRA or annuity at this time.

Because these distributions often involve complex analysis of income and tax scenarios to determine the best choice for your unique circumstances, it's wise to consult your financial professional.

If you have substantial assets that generate more income each year than you spend, you may want to consider investing in a variable annuity. Your investment earnings will grow and compound tax deferred until withdrawal. However, when you withdraw earnings, they are taxed as ordinary income regardless of how long they have accrued in your account. Because these tax rates may be higher than capital gains tax rates, you may want to use variable annuities for your fixed-income investments and your most aggressive stock investments -- those that typically experience high turnover and therefore generate substantial short-term income distributions (which are taxed as ordinary income rather than as long-term capital gains).

Annuities also allow you to continue making contributions after retirement and to defer withdrawals, often until age 80 or later. Withdrawals from traditional, non-Roth IRAs, however, must begin no later than April 1 following the year you turn 73. After that, you must make your second withdrawal by December 31 of that year and future withdrawals by each of the subsequent December 31 dates.

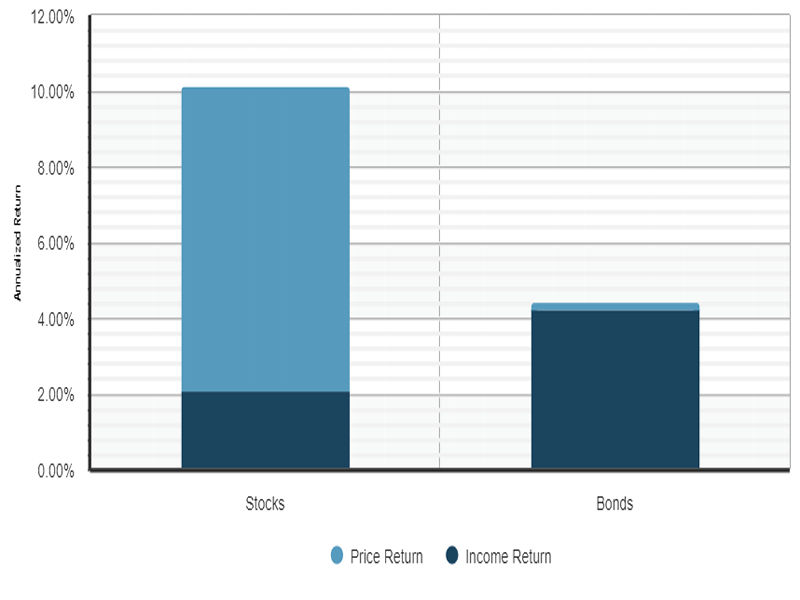

| Components of Total Return |

|

| While stocks have historically provided income and capital

appreciation, the total return of bonds has been composed primarily

of interest income. Past performance is not indicative of future

results. Source: ChartSource®, SS&C Retirement Solutions, LLC. For holding periods for the thirty years ended December 31, 2023. Stocks are represented by the S&P 500 index. Bonds are represented by the Bloomberg U.S. Aggregate Bond index. It is not possible to invest directly in an index. Index performance does not reflect the effects of investing costs and taxes. Actual results would vary from benchmarks and would likely have been lower. Past performance is not a guarantee of future results. © 2024 SS&C. Reproduction in whole or in part prohibited, except by permission. All rights reserved. Not responsible for any errors or omissions. (T2P30S) |

Donate Appreciated Assets to Generate Income

You can donate highly appreciated assets to charity and generate current income, along with a tax deduction, using a charitable remainder trust. With the top capital gains tax rate at 15% for most investors, the value of the tax deduction may be less than in previous years but could still provide an advantage to wealthy individuals.

A charitable remainder trust requires that you donate the asset to a qualified charity or foundation, which will establish a trust. The trustee sells the asset at market value, invests the proceeds, and pays you annual investment income. You receive a current tax deduction based on the expected remainder value of the asset and your life expectancy. At your death, the trust is paid to the designated charity.

Develop a Strategy for Income and Growth

An investment portfolio can work hand-in-hand with retirement accounts, annuities, and trusts to meet your income and growth needs. To help determine what kind of investment vehicles may be appropriate for your particular circumstances (as well as how much of your portfolio should be allocated to each asset class), consider your risk tolerance and your needs for income vs. growth. You also want to consider the tax consequences of each option. Your financial professional can help you find a balance that is appropriate for you. Once you've established a suitable portfolio, you might consider using your fixed-income and money market investments1 -- and any retirement plan and trust distributions -- for your annual expense money. Of course, continuous attention to detail can help keep you ahead of the game -- and well cushioned against the rising cost of living.

1An investment in a money market fund is not insured or guaranteed by the Federal Deposit Insurance Corporation or any other government agency. Although most funds seek to preserve the value of your investment at $1.00 per share, it is possible to lose money by investing in a money market fund.

2Share prices may fall in value as well as increase, and there is no assurance that the full value of an investment in stocks can ever be recovered.

3Bond values are not guaranteed. A bond's market price may vary significantly from face value. Investors may receive the face value or redemption value of a bond only if it is held to maturity or call date. High-yield bonds present greater risk of default.